June 17th 2024

At the start of every month, our real estate boards publish the sales stats for the previous month. It’s always interesting to see these figures and from them try to deduce where the market is going based on past and current performance.

The Niagara stats are now in, and while there are a number of factors reported, we specifically zero in on two: the average residential sale price and the number of residential sales recorded.

According to these most recent stats, the average residential sale price for May came in at $706,771. That’s up $11,140 or 1.60% from April and up $62,704 or 9.74% from the $644,067 recorded at year end 2023.

Based solely on these figures we would think that we are seeing a pretty strong recovery. I mean almost 10% price increase in less than half a year is substantial. But that in and of itself is not an accurate indication of where the market is headed. First, we need to look at each municipality and see how they are behaving. The two largest municipalities in our region are St. Catharines and Niagara Falls. In May, St. Catharines average price was up $14,425 or 2.32%, while Niagara Falls was down $25,203 or 3.77%. Mixed signals. And that’s what we see across the Region. Of the 10 municipalities tracked, 6 are up month over month and 4 are down. And in some cases, there swings are sizeable. Fonthill/Pelham for example was up $121,953 while Thorold on the other hand was down $110,567. That suggests that the market overall is unsettled and giving very mixed messages.

To better understand what is actually going on, we need to step back a little and expand the picture. The region as we’ve seen came in for May 2024 at $706,771. But exactly one year ago May 2023 the average stood at $705,929. That’s a year over year difference of only $842. Virtually unchanged statistically.

What we have seen both last year and this to date is an upward trend in prices during the first half of the year (spring market) followed by a settling down over the second half of the year. In fact, when we look regionally at the period from January 2023 to today, we see the averages varying from a high of $736,491 to a low of $627,561 with today’s numbers settling mid-way between.

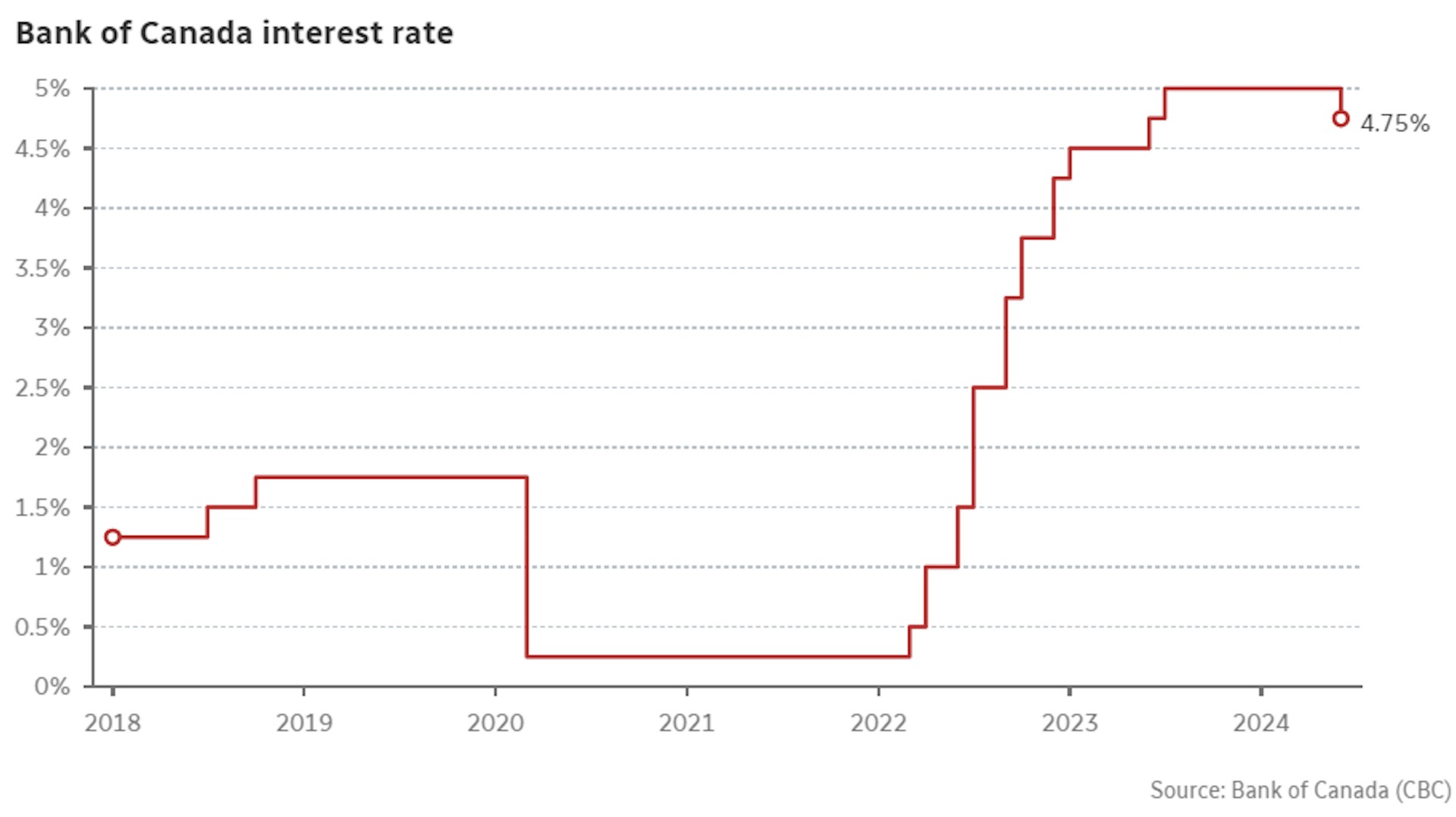

I think to understand what is actually happening and why, we need to take a good hard look at interest rates. Because they, more than any other factors, are what is driving the shifts in the marketplace.

Rolling the clock back to the onset of Covid. In March 2020 the Bank of Canada’s key interest rate was sitting at 1.75%. Then Covid hit and in response the Bank of Canada slashed its interest rate by 1.50% down to an almost unprecedented 0.25%. Basically ‘free’ money. And in real estate the market responded with one of the greatest buying sprees in history. Over the next 2 years the Bank of Canada held rates steady at 0.25% and as a result everybody, investors, speculators, renovators and end users had a heyday. You know the results. Multiple offers, bidding wars and colossal price gains. Until March 2022. And that’s when the Bank of Canada stepped in and started to rachet up interest rates.

From March 2022 to year end interest rates were constantly revised from 0.25% right up to 4.25%. And the net result was that real estate took it on the chin with plummeting prices, plummeting activity and a lot of bewildered consumers. So, while we tend to attribute the boom to Covid, it was actually pretty well interest rate driven.

So now, June 5, 2024, the Bank of Canada cut their key interest rate by 0.25%. Not all that significant. I mean ¼% isn’t going to impact anybody’s buying power by all that much. But what is significant is the downward trend. This is the first rate cut since March 2020. That’s over 4 years. The Bank promised rate cuts would be seen by the 2nd quarter of 2024 and that’s exactly what they have done. And they are strongly hinting at more to come.

CIBC economist Andrew Grantham states that he expects the Bank of Canada to lower interest rates by another 25 basis points at it’s next meeting, on July 24th, with another two cuts after that before the end of the year. He’s probably not wrong.

It’s a tough balancing act for the Bank of Canada. Hold off on rate cuts and you essentially strangle the economy. Quarterly GDP numbers released at the end of April were weaker than expected. The economy grew by only 1.7% during the first three months of the year. At the same time, the inflation rate has moved down closer to the bank’s two percent goal in recent months, coming in at 2.4% in April, with the Bank’s preferred core measure of inflation also easing throughout the spring. But drop rates too quickly and inflation could well spiral out of control. In the words of BOC governor Tiff Macklem “The Bank of Canada is going to take things one meeting at a time. Canadians can reasonably expect more cuts so long as inflation continues to ease, and the Bank maintains its confidence that inflation is steadily approaching the Bank’s two percent goal.”

So, moving forward, we’ll continue to watch and report the key indicators of price and unit sales. But expect no significant change until interest rate cuts become clearly established as a downward trend. How many cuts before that registers with the consumer remains to be seen, but when it does, you can expect to see consistent upward trends once again in both price and sales volumes.

In the words of Tu Nguyen, an economist with RSM Canada:

“A single rate cut won’t revive the economy overnight, but it signals to consumers and businesses the beginning of a gradual and orderly rate cut cycle that will unfold over the next year and a half. Recovery can begin now and hit full force in 2025.”