July 15th 2024

To really understand the Canadian economy today especially as it is reflected in the Real Estate market, you need to travel back in time to the late 1970’s and early 1980’s. Two factors need to be analyzed. Inflation rates and interest.

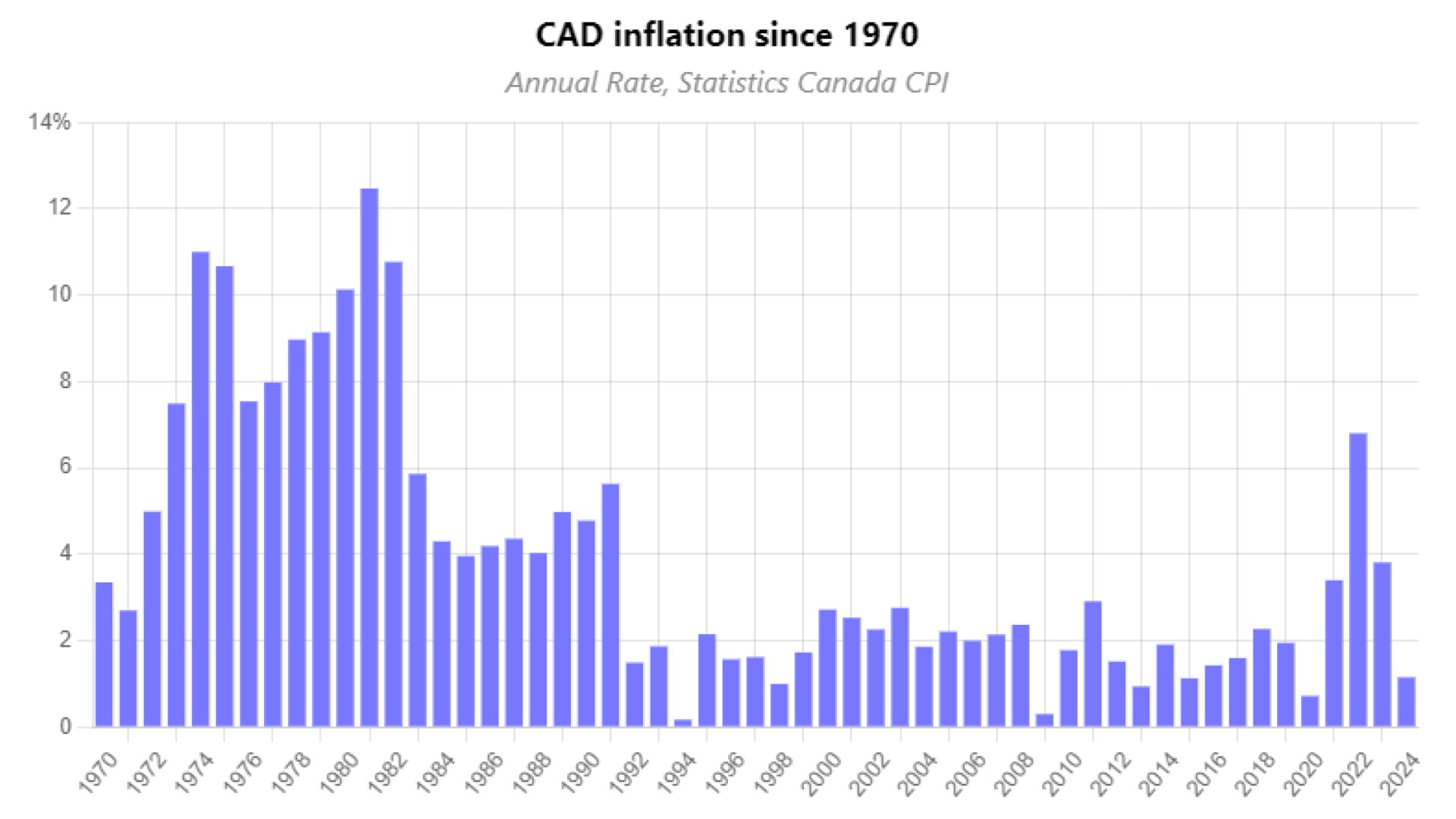

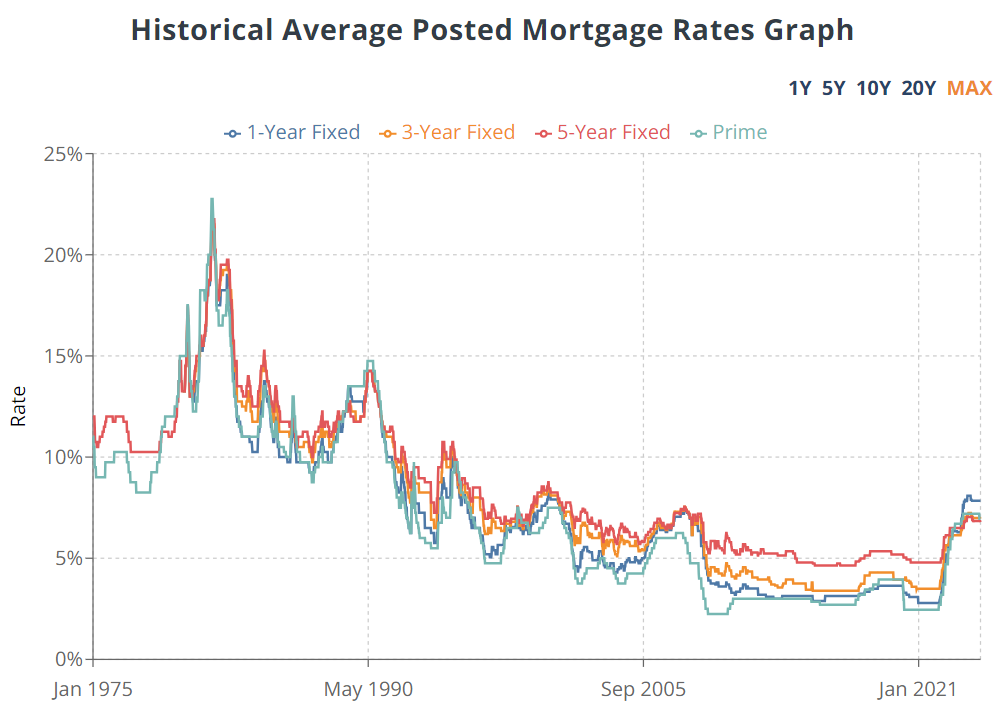

During the era of the 1970’s we saw interest rates for 5-year mortgages rise generally from 7.5% to end the decade at 13.25%. Not quite doubling, but close. But to really understand the story we need to look at inflation. Inflation during the decade of the 70’s was on the rise. By 1978 inflation in Canada was running at 8.97%. It crept up in 1979 to 9.14% and in 1980 it rose again to 10.13%. But it didn’t stop there. By 1981 inflation had peeked at 12.47%. Understandably that was troubling to economists and especially to the Bank of Canada.

They stepped in. What did they do? They began to combat inflation by ratcheting up interest rates. And they were ruthless about it.

As we’ve seen, the decade of the 70’s ended with interest rates at 13.25%. By 1981 the Bank of Canada had raised prime to 22.75%. In October 1981 5-year mortgage rates were running at 21.75%. This of course crippled the economy. Businesses that were operating with credit lines simply went out of business. They couldn’t sustain the cost of operations with the crippling cost of money. Bank managers had jars on their desks where people could simply give up and drop off the keys to their houses and cars. But it did have the desired effect on inflation. Inflation which was running at 10.77% in 1982 fell to 5.86% by 1983 and down to 4.30% by 1984. And with the easing of interest rates came a rebound to the economy. Especially evident in Real Estate. 1984 saw the real estate market pick up steam and that trend strengthened moving ahead. By 1986 the real estate was in balanced territory, and a couple of years later it was hot. Prices were spiking and so were sales. People were lined up to buy and in competition for houses.

So here we are 45 years later in the exact same cycle. Inflation ran at a very modest rate pretty well throughout the 2010’s. June 2019 for example it sat at 1.9%. A year later, in June 2020 it hovered at 0.7%, the starting period of Covid, remember, where the market began to really heat up. By June 2021 it was running at 3.6% and by June 2022 it had hit a startling 8.1%. And what did the Bank of Canada do? You guess it. Stepped up and began to rapidly rachet up interest rates. And it had the expected results. It brought down inflation which by June 2023 was reduced to 2.8%, but it also crippled the economy. People who had brought houses with mortgages under 2% were looking at renewal rates in the 6% range. House payments were doubling and in some cases tripling. Thankfully we are now in a downward trend with interest rates. By historic standards, this peak was actually quite low. And as they fall, we will see a point when the fulcrum will shift and the stamped will start again with frantic buying and huge price escalations. We aren’t there yet, but we are well on our way. I think the recovery will be gradual at first, and although I’m in real estate and therefore expected to say it, I truly believe we are at a wonderful place to capitalize on this recovery cycle. Prices haven’t yet risen to any consistent extent. Interest rates are affordable and by starting with a variable product you can lock in at tomorrow’s lower rates while having bought at today’s relatively bargain price.