August 15th 2024

As we watch the sales figures come in month by month and year by year, there are a couple of trends we need to keep in mind. The first is cyclical. What is happening seasonally? And the other is economic. What is happening overall due to market pressures brought about by interest rate fluctuations and inflationary changes?

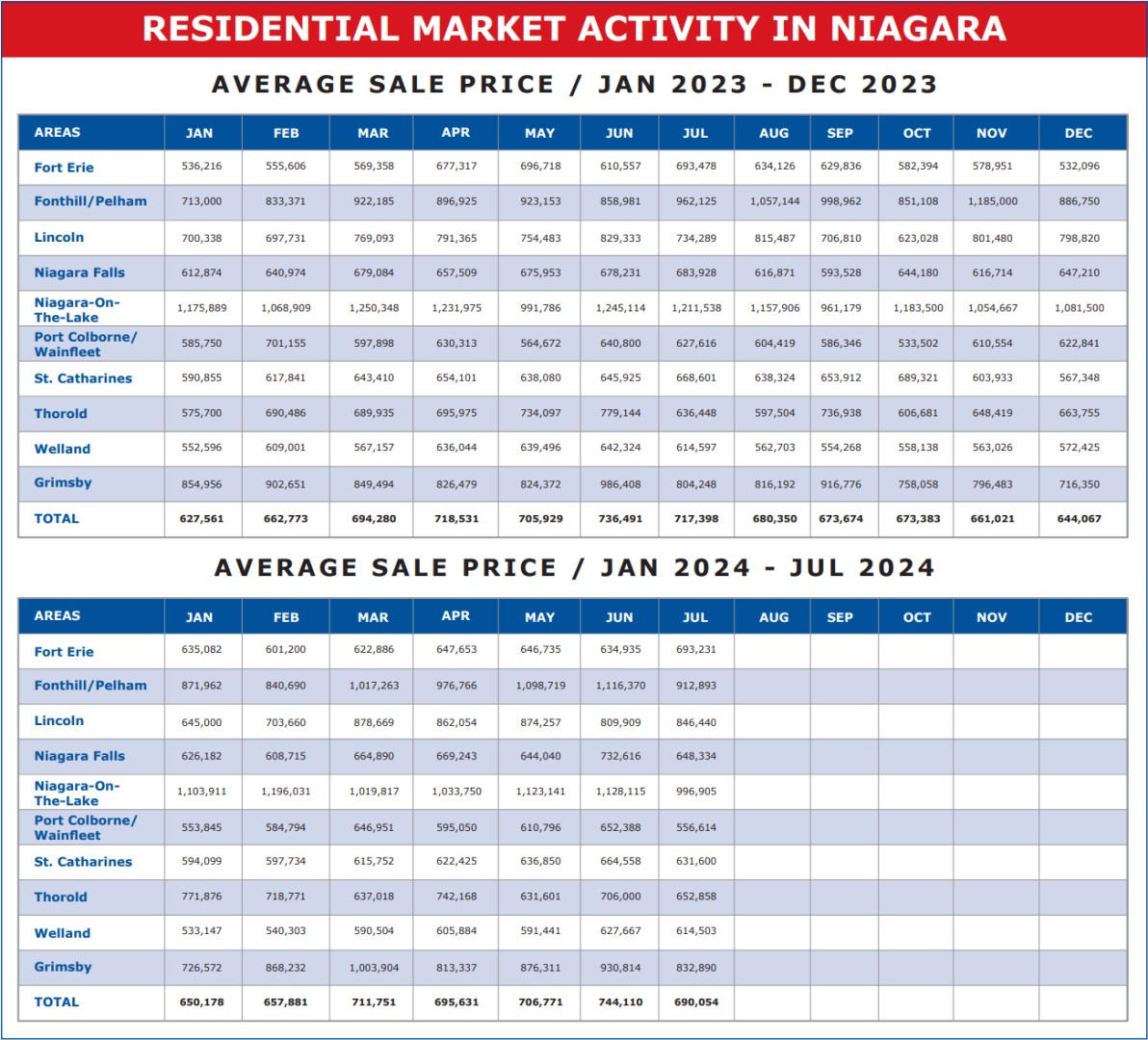

But before we attempt to understand the market shifts, let’s begin by looking at the raw data. And I’d like to draw your attention to the average sale price across the region, first on a monthly basis over 2023 and then over the first 7 months of 2024.

We often refer to the ‘spring market’ as the time when the market heats up. Of course, that is not always the case. Boom and bust cycles don’t always follow the calendar. But all things being equal, there is evidence of the market strengthening over the busy spring. To illustrate, let’s look at the two most recent years 2023 and 2024.

The year 2023 saw the market open up across the Niagara region with the average sale price in January coming in at $627,561 (Down nearly $30,000 from where the market ended the year 2022). Over the next 6 months ending June 2023 the average sale price increased every month except one (May) and ended the first half year at $736,491. That’s a six month increase of $108,930 or 17.36%. But look what happened beginning in July. July 2023 saw prices slip by $19,093 or 2.59%. And that downward trend continued every single month to the end of the year, with December 2023 recording an average sale price of $644,067, down $92,424 or 12.55% from June. Erasing all but $16,506 of the over $100,000 gained in the spring.

Now, let’s take a look at this year, 2024. We began the year with an average sale price in January of $650,178. Then, over the next 6 months, we saw average price gains every single month but one (April), ending the first half of the year at $744,110. A gain of $93,932 or 14.45%. Nice. Then along came July, and average prices dropped to $690,054, a one month decline of $54,056 or 7.26%. Or to put that in clearer perspective, June 2024 compared to June 2023 was up year over year $7,619 while July 2024 compared to one year ago July 2023 is down $27,344. In other words, based on the first month of the second half of 2024 we’re losing ground faster than we did in the comparable period last year.

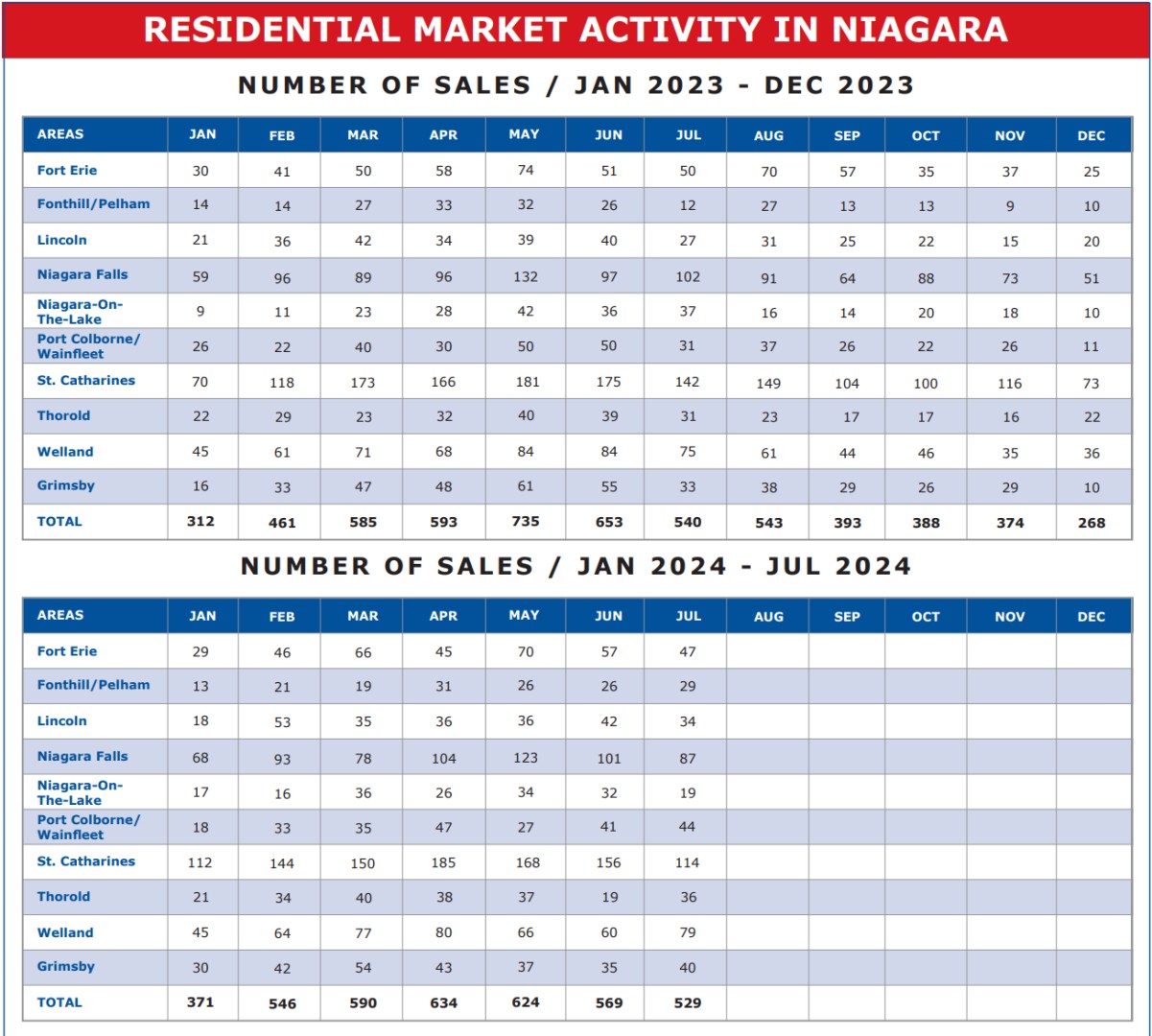

Of course, one month does not a trend make. Quite puzzling however is when you weigh these changes in the light of the economic forces we talked about earlier. Over the past couple of months in 2024 we have seen the bank lower rates twice. That didn’t happen at all in 2023. So, shouldn’t that have the reverse effect? Shouldn’t we see an increase in prices as a result, or at the very least a slow down of the decline? One would think so. But not the case. One factor that will help shed light on what is going on is unit sales. Let’s take a look at the number of sales, month by month since January 2023.

In the first four months of 2024, each month outperformed the previous years corresponding monthly figures. Jan. 371 vs 312, Feb. 546 vs 461, Mar. 590 vs 585 and Apr. 634 vs 593. That’s a four-month difference of 190 units, an increase of 9.74%. The market was strengthening. People were becoming more confident and getting back into the market. But look at May-July. In 2023, 1,928 residential properties changed hands, while over the same three-month period in 2024, that total has dropped to 1,722. A decline of 206 units or 10.68%. What changed? Interest rates. The Bank of Canada began to drop interest rates and buyers began to hold off and take a ‘wait and see’ approach.

Here again this isn’t totally surprising. In our last month’s newsletter, we took a look at the real estate market in the early 1980’s. You will recall we saw staggering inflation rates about that time and incredible interest rate hikes brought into play to combat that trend. Shortly thereafter the Bank of Canada slashed interest rates drastically and rapidly, but the market still took 4-5 years to recover.

I don’t expect to experience that sluggish a recovery this time around. Primarily because we didn’t see anywhere near the interest rate hikes recorded in the early 80’s. And back then, a moderation brought mortgage rates to around 10%-11%. Still relatively high! Today, with only a few 1/4 point drops we’ll be back to very affordable borrowing rates certainly under 4%. People will only sit on the sidelines for so long. I believe at some point in the not-too-distant future with rates continuing to decline we’ll see the fulcrum tip and when that happens the buyer floodgates will open wide.