December 16th 2024

The market report is going to be a little thin this month I’m afraid. Especially when it comes to specific data. The Niagara Association of Realtors (NAR) which we look to for our raw sales data is in the process of changing MLS data systems and the numbers for November are not currently available.

Having said that, as we draw towards the end of the year, there are certain conclusions we can draw from our internal sales statistics here at RE/MAX Garden City Realty Inc.

Each month our sales boards record the activity as it unfolds in each of our offices. Although this is a mixture of conditional as well as firm sales, and in fact includes lease activity, it is consistent in its composition month by month and year by year. In the month of November for example, we recorded a significantly higher number of sales events than we did one year ago (up 54.7%). And this has been consistent month by month over the entire year. In fact, there was only one month (February) where 2024 was lower than the corresponding month one year ago. And that was only lower by one sale. The other 10 months came in higher than the corresponding month last year, and overall were up a surprising 31.8% year to year January to November.

So, while probably not quite as extreme as the production surge we are enjoying this month, it’s certainly safe to draw two conclusions that apply to the overall market. One is that overall, 2024 is certainly stronger in sales than was 2023. And secondly, the market is remaining surprisingly active right into November. In fact, here at RE/MAX Garden City Realty our sales activity in November is the strongest it has been in years, coming in even higher than the unit sales in 2021 when the market was at its frenzied peak.

There has been a lot of interest in the real estate market, right through the post covid era, and while for the last 2 ½ - 3 years a lot of people have been watching from the sidelines, they are beginning to jump back in. December and early January are traditionally slow periods. People have different priorities that time of year. But I expect to see activity pick up substantially as early as mid-January and certainly into the spring.

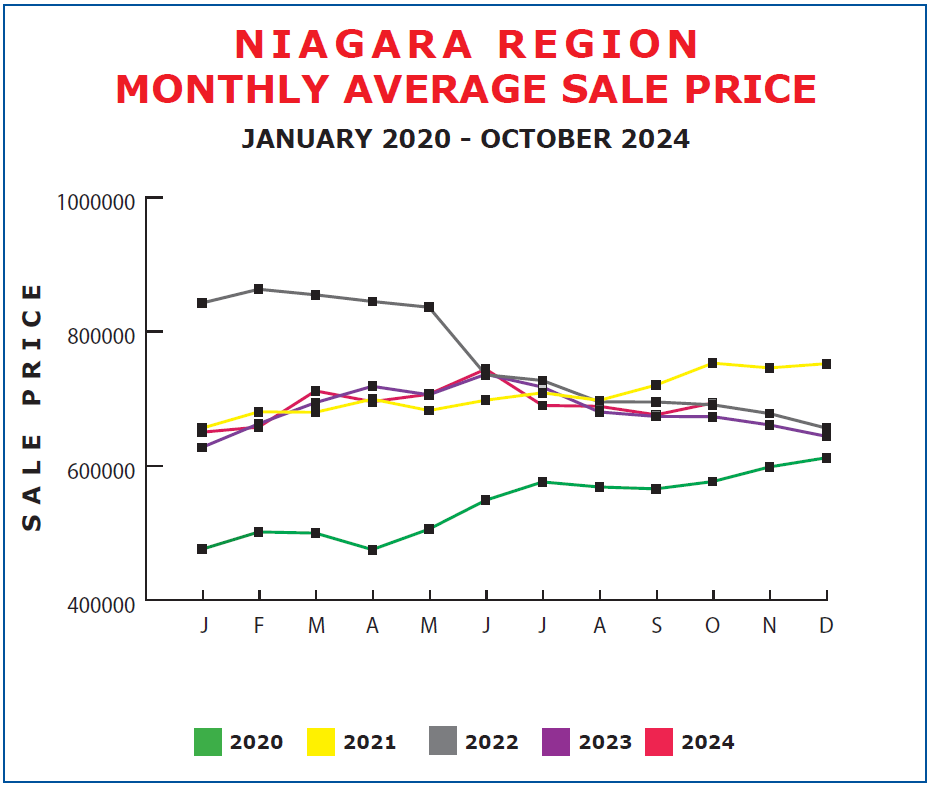

But what about prices? What’s happening there? Again, due to the changes at the Board I can’t provide any hard data for November, but I can spot overall trends occurring over the last couple of years on a year-by-year basis.

2020 to 2022 were unusual years to say the least with the frenzied run-up of prices during covid and the remarkable loss of much of those gains in the period since. But what we have certainly seen both in 2023 and to date in 2024 are remarkable gains in the first 6 months of each year followed by substantial drops in average sale prices over the last 6 months of the year.

However, there are a couple of significant differences in the price slide over the last half of 2023 and that of 2024. If we look at June to July in 2024 the average price dropped by an alarming $54,056 compared to only $19,093 during that one-month period in 2023. But then the trend changed. From July to October 2023 the market slid a further $44,015, and yet in that same period in 2024 the market slid slightly from July to September (-$13,980) but it actually gained back all those losses in October coming in $3,690 higher than July.

So, in summary, I see the market certainly picking up in activity and I expect that trend to continue. And along with that, we’re seeing the inevitable fall price slide slowing in 2024 and I think that is foretelling an encouraging uptick in prices throughout 2025.